News

We provide the latest news from the world of economics and finance

We provide the latest news from the world of economics and finance

JPMorgan Chase & Co. JPM remains well-positioned for growth on the back of higher rates, strategic acquisitions and restructuring initiatives, and a resurgence in global deal-making activities. However, challenges in improving fee income because of high mortgage rates and volatile capital market revenues are woes.

JPMorgan’s net interest income (NII) and net yield on interest-earning assets are likely to experience decent growth as the Federal Reserve is expected to keep interest rates high in the near term. However, rising funding and deposit costs will continue to exert pressure on both to some degree. Though NII dipped in 2020 and 2021 amid the low interest rate environment, the metric reflected a five-year (2018-2023) compound annual growth rate (CAGR) of 10.1%. This rise was partially driven by the First Republic Bank’s acquisition in 2023. Similarly, net yield on interest-earning assets expanded to 2.70% in 2023 from 2% in 2022. The uptrend for both metrics continued during the first quarter of 2024 on a year-over-year basis. The company projects NII in 2024 to rise roughly 2.5% to approximately $92 billion.

Despite the rapid growth of mobile and online banking options, JPM remains focused on its footprint expansion in new regions. In February 2024, the company announced plans to open more than 500 new branches by 2027 to strengthen its position as the bank with the largest branch network and a presence in all 48 states of the United States. The company commenced its digital retail bank Chase in the U.K. in 2021 and intends to expand the accessibility of its digital bank across the European Union. JPMorgan is also focused on strengthening the Commercial & Investment Bank (CIB) and Asset & Wealth Management businesses in China.

While global deal-making activities nearly came to a grinding halt at the start of 2022, JPMorgan remained a top-ranked entity in terms of global investment banking (IB) fees. While the company’s total IB fees (in the CIB segment) slumped 59% in 2022 and 5% in 2023, the company has been observing encouraging signs within the business. During the first quarter of 2024, IB fees surged 21% on a year-over-year basis, with the company holding a market share of 9.1%. The company is expected to see growth in IB fees going forward, given a healthy IB pipeline and active merger & acquisition (M&A) market. It also intends to leverage its top position to amplify the magnitude of the gain due to the changed scenario.

JPMorgan has been expanding via both domestic and global acquisitions. Last year, the company increased its stake in Brazil’s C6 Bank to 46% from 40%, established a strategic alliance with Cleareye.ai, a financial technology firm focused on trade finance and acquired Aumni and First Republic Bank (an FDIC-assisted deal). These deals, along with several others in the past, are likely to keep aiding the bank’s plan to diversify revenues and expand fee income product suite and consumer bank digitally.

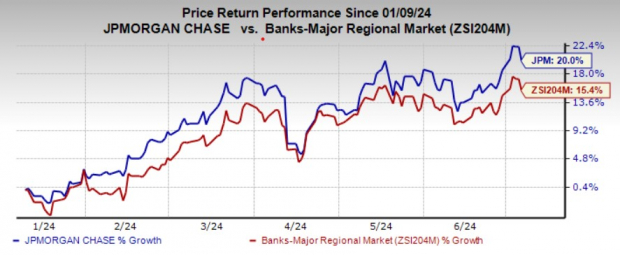

JPM currently carries a Zacks Rank #3 (Hold). In the past three months, shares of the company have gained 20% compared with the industry’s growth of 15.4%.

Image Source: Zacks Investment Research

Nonetheless, JPMorgan’s excessive reliance on the performance of the capital markets to generate fee income is a matter of concern. Though increased volatility and a surge in client activity in 2022 led to improved trading performance, the same normalized on a gradual basis thereafter. The market's revenues dipped 4% on a year-over-year basis in 2023, with the trend continuing during the first quarter of 2024. The volatile nature of the business is likely to make growth challenging moving forward.

JPM’s mortgage fees and related income performance turned dismal amid the continued rise in mortgage rates since 2022. This led to subdued demand for mortgage loans and refinancing. The metric witnessed a negative CAGR of 27.5% over the three years ended 2023. While the trend reversed during the first quarter of 2024, origination volumes and refinancing activities are unlikely to experience solid growth as mortgage rates are likely to stay elevated in the near term.

Some better-ranked banking stocks worth a look are Northrim BanCorp, Inc. NRIM and Bank of Marin Bancorp BMRC, each sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks Rank #1 stocks here.

The Zacks Consensus Estimate for NRIM’s current-year earnings has been revised 12.2% upward in the past 60 days. The company’s shares have risen 5.3% in the past six months.

The Zacks Consensus Estimate for BMRC’s current-year earnings has been revised 5.7% upward in the past week. The company’s shares have lost 22.7% in the past six months.

Zacks Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

JPMorgan Chase & Co. (JPM) : Free Stock Analysis Report

Northrim BanCorp Inc (NRIM) : Free Stock Analysis Report

Bank of Marin Bancorp (BMRC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd is authorised and regulated by the Cyprus Securities and Exchange Commission in accordance with license No.281/15 issued on 25/09/2015. The "Just2Trade" trademark is owned by LimeTrading (CY) Ltd.

Registration Number: HE 341520

Address: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Disclaimer:

All promotions, materials and information of this website may have applied conditions. Please contact the Company for further details

Trading on financial markets carries risks. The value of the investments can both increase and decrease and the investors may lose all their investment capital. In case of a leveraged product, the loss may be more than the initial capital invested. Detailed information on risks associated with trading on financial markets can be found in General Terms and Conditions for the Provision of Investment Services.

E-mail: 24_support@just2trade.online