News

We provide the latest news from the world of economics and finance

We provide the latest news from the world of economics and finance

Spectrum Brands Holdings Inc. SPB seems well-poised for growth, thanks to its robust strategic efforts. The company is benefiting from increased pricing, cost improvements and a favorable mix. Its Global Productivity Improvement Plan (“GPIP”), which aims at improving operating efficiency and effectiveness, appears encouraging too.

The company is on track with the four core pillars to drive growth. In this regard, it is streamlining its organizational structure and re-energizing its employee base. SPB is committed to improving operational efficiencies while limiting risk. Management is protecting and deleveraging its balance sheet while solidifying liquidity. It is focused on transforming the company into a pure-play global Pet and Home & Garden business.

Spectrum Brands’ initiatives like pricing, cost improvements and a favorable mix have been driving margins for a while now. The company has been proactive in its cost-takeout actions, which were implemented in the second half of fiscal 2022, including fixed cost reduction by eliminating permanently salaried headcount and reducing advertising and promotional spending.

Image Source: Zacks Investment Research

Further, the company’s GPIP is focused on consumer insights and growth-enabling functions, including technology, marketing and research and development. This plan will also enable it to deliver value creation and sustainable growth in the long term. In addition, the company is focused on delivering savings, the majority of which are expected to be reinvested into growth initiatives.

However, Spectrum Brands has been witnessing soft demand in the small kitchen appliances category, volume declines in certain pet channels and the impact of SKU rationalizations. This, along with the difficult consumer environment, somewhat impacted the company’s results in second-quarter fiscal 2024. The top line fell 1.5% year over year while organic net sales dipped 1.6%.

In addition, the company’s Home & Personal Care segment continues to be sluggish. Sales for the segment dipped 4% year over year in the fiscal second quarter due to lower sales in small kitchen appliances.

Nevertheless, the aforesaid strengths are likely to continue to boost overall growth. Looking ahead, Spectrum Brands projects reported sales to remain flat year over year in fiscal 2024. Adjusted EBITDA, excluding the investment income, is likely to grow in the low-double digits for the fiscal year.

Analysts seem quite optimistic about this Zacks Rank #3 (Hold) company. The Zacks Consensus Estimate for fiscal 2024 sales and earnings per share (EPS) is currently pegged at $2.92 billion and $4.68, respectively. These estimates indicate corresponding growth of 0.1% and 205.9% year over year.

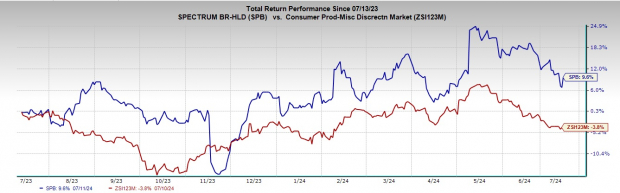

Driven by such upsides, the stock has gained 9.6% in the past year against the industry’s 3.8% decline.

We have highlighted three better-ranked stocks, namely, G-III Apparel Group GIII, Crocs CROX and Royal Caribbean RCL.

G-III Apparel is a manufacturer, designer and distributor of apparel and accessories under licensed brands, owned brands and private label brands. It sports a Zacks Rank #1 (Strong Buy), at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

GIII Apparel has a trailing four-quarter earnings surprise of 571.8%, on average. The Zacks Consensus Estimate for GIII Apparel’s current financial-year sales indicates growth of 3.4% from the year-ago figure.

Crocs develops and manufactures lifestyle footwear and accessories. It currently has a Zacks Rank #2 (Buy). The company has a trailing four-quarter earnings surprise of 17.1%, on average.

The consensus estimate for Crocs’ current financial-year sales and EPS implies an improvement of 4.3% and 5.6%, respectively, from the prior-year actuals.

Royal Caribbean carries a Zacks Rank of 2, at present. RCL has a trailing four-quarter earnings surprise of 18.3%, on average.

The Zacks Consensus Estimate for RCL’s 2024 sales and EPS indicates an increase of 16.8% and 63.8%, respectively, from the year-ago reported levels.

Free Report: 5 “Whisper” Stocks Poised to Stun Wall Street

Analysts may be seriously underestimating these stocks. When they announce earnings, they could immediately jump +10-20%.

See Stocks Now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

G-III Apparel Group, LTD. (GIII) : Free Stock Analysis Report

Spectrum Brands Holdings Inc. (SPB) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd is authorised and regulated by the Cyprus Securities and Exchange Commission in accordance with license No.281/15 issued on 25/09/2015. The "Just2Trade" trademark is owned by LimeTrading (CY) Ltd.

Registration Number: HE 341520

Address: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Disclaimer:

All promotions, materials and information of this website may have applied conditions. Please contact the Company for further details

Trading on financial markets carries risks. The value of the investments can both increase and decrease and the investors may lose all their investment capital. In case of a leveraged product, the loss may be more than the initial capital invested. Detailed information on risks associated with trading on financial markets can be found in General Terms and Conditions for the Provision of Investment Services.

E-mail: 24_support@just2trade.online