Opciones individuales soluciones

Take advantage of the features of futures options without having to go through complex

mathematical formulas.

We offer several categories of solutions.

Within each category, only a small number of solutions are provided, primarily for the purpose of illustrating ideas. The number of possible option solutions is practically unlimited.

Las tasas globales han aumentado. Muchos bancos no pagan intereses comparables sobre los depósitos. Para obtener una buena tasa en un depósito, generalmente es necesario elegir un plazo largo sin la posibilidad de retirar el depósito. Muchos corredores de futuros no pagan intereses sobre los saldos o pagan una tasa desproporcionada.

Solución.Ciertas soluciones de opciones proporcionan rendimientos fijos comparables a la tasa actual del mercado..

En este caso:

Existe una previsión de cambios en los precios de un activo en un horizonte determinado. Hay una selección de soluciones de opciones sobre cómo calcular el pronóstico. Pero estas soluciones no son gratuitas, sino que requieren el pago de primas de opciones.

Solución.La combinación correcta de las estrategias en la Solución 1 y las soluciones de opciones proporciona una solución "gratuita" que compensa el pago de las primas de las opciones.

Hay un pronóstico de movimiento bastante fuerte para el día.

Solución.Se compra una opción de hoy (con fecha de vencimiento hoy) con la esperanza de que el pronóstico se haga realidad. En este caso, se pueden lograr ganancias que son múltiplos de la prima gastada.

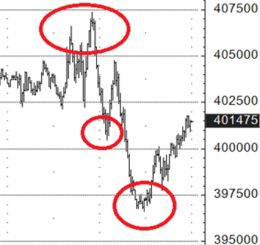

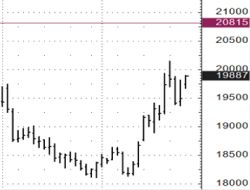

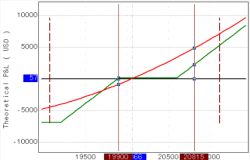

E-Mini S&P 500 Futuros.

En la zona del tope hubo una compra del puesto de hoy (con vencimiento hoy) con un strike de 4000 por 1,00 puntos (50 dólares). En el primer" empujón " hacia abajo, la opción costó 20,00 puntos( 1.000 dólares), es decir, 20 veces la prima pagada. Al comienzo del segundo" empujón", la opción costaba 34,00 puntos (1.700 dólares), es decir, pagaba 34 veces la prima.

There is an opinion that it is necessary to limit losses by placing stop orders, the so-called “stop loss”. In this case, the stop order may be executed, but the market then turns in the direction of the original position, which, in the end, could even be profitable.

Solution.Using options as an alternative to stop loss. A stop loss implemented in this way gives the position a greater chance of returning to the profitable zone and eliminates losses associated with gaps beyond the stop loss level.

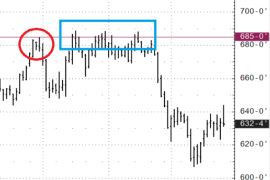

"Stop Loss". Corn futures.

There is a short position in a futures (sold futures). The stop loss level was chosen above the high of 685-0 (red circle). If there was a stop order at 685-0, it would have been triggered (blue area). At the same time, in the end, the market fell and would have brought profit. But the trader was left without a position. Buying a call option with a strike price of 685-0 with sufficient time until expiration would guarantee protection above the 685-0 level, while leaving the position open to profit in the event of a fall. The trade-off for staying in the position is paying an option premium, which would increase losses above the 685-0 level if the market closed above that level on the expiration date.

"Gap". Oil futures.

There is a short position in a futures (sold futures). The stop order is at 76.00, limiting potential losses. However, significant news came out over the weekend and the market opened with a “gap” and the stop order was executed at a price of 80.10, realizing additional losses. If, instead of a stop order at 76.00, a call option with a strike price of 76.00 had been purchased, it would have guaranteed the position to be closed at 76.00. In this case, the maximum additional loss would be limited only by the option premium, which would be significantly better compared to an executed stop order at a price of 80.10. Moreover, since using an option as a “stop loss” there is no need to close the position, there was still a chance (if there was enough time before the option expiration) to wait for the fall and realize the profit as a result.

There is a forecast of changes in prices for an asset over a certain horizon. At the same time, you don’t want to lose in the range of current prices.

Solution.Option solutions allow you to achieve break-even or a small profit within a given range of price changes.

In this case:Oil futures.

Current price 71.00. The forecast period is 3 months. The break-even range is 59.70 and above. If you just buy futures, the break-even range is 71.00 and above.

There is a forecast of levels for the day and the likelihood of their achievement. It is not clear what is the best way to work out this forecast.

Solution.Use of so-called Event contracts on CME, which represent binary options. These are fixed bets with fixed maximum profits and losses.

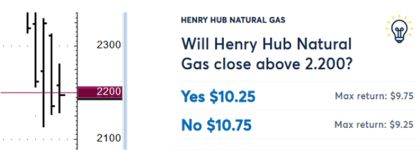

Futuros de Gas Natural.

Pronóstico: Los futuros no cerrarán por debajo de 2.200 hoy. Dicho contrato se compra y se pagan0 10.75. El pago máximo según el contrato es de0 20.00. Y si el mercado cierra por encima de 2200, el contrato pagará $20.00, lo que significa profit 9.25 en ganancias (20.00 recibidos menos paid 10.75 pagados).

There is a forecast of changes in prices for an asset over a certain horizon. There is a desire to work out the situation by purchasing an option. Profit on the expiration date is realized only if the asset closes above (if a call is purchased) or below (if a put is purchased) the option strike. And you will need to deduct the premium paid.

Solution.The use of option combinations that allow you not to lose paid premiums in the range from current prices to the strike price. The trade-off is increased losses when prices move from current levels in the opposite direction to the forecast.

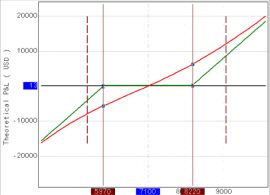

Gold Futures.

Forecast: Futures will rise. You can buy a call with a strike of 2060 at a price of 21.50. Moreover, on the expiration date, profitability will be achieved only at a level above 2081.50. Below these levels there will be a loss.

By adding several other options, you can get the following configuration: The price at which losses begin is moved below 1990.00. Trade-off - losses increase below 1990.00 compared to the limited losses of 21.50 points in the situation of just buying a call.

There is a position that is not developing according to plan - it is unprofitable. The position would happily be closed at breakeven, but the market has moved relatively far from the breakeven price. Often traders try to “fight back” using the so-called “averaging”: an additional purchase of an asset in the case of a long losing position or an additional sale of an asset in the case of a short losing position. Thereby bringing the break-even price closer. The problem is that the risk increases in the event of further unfavorable price movements.

Solution.Use of option combinations that allow you to move break-even price closer to current market prices. At the same time, the risk in the event of further unfavorable price movements does not increase.

Gold futures.

A long position was opened at 2050.00 (red circle). An option combination has been added at the price (green circle). Which made it possible to reduce the breakeven price to 2022.10 on the options expiration date without increasing the downside risk. Compromise - there is no profit potential above the price of 2022.10.

There is a forecast of the price level for entering a position. But the price may not reach there.

Solution.An option is sold with a strike at the level of the price entry into the position. If the price is outside the strike price on the expiration date, the option is exercised into the futures and a resulting futures position is obtained. At the same time, the opening price was improved by the amount of the option premium received. If the price does not reach the strike level, the premium received from selling the option is retained. Compromise - if the price “moved” beyond the strike and then returned on the expiration date, the option will not be exercised and there will be no futures position.

Sugar futures.

When prices are in the green rectangle, an upward trend is identified. The entry point is determined at the level of the blue rectangle. A put is sold with a strike at the level of the blue rectangle (1700). If on the expiration date the price was below 1700, the put would be executed on the futures and a long position would be opened (futures purchased) at 1700. In this case, the purchase price would be improved by the amount of the premium received from the sale of the put. In the real situation, the market did not reach the strike levels. The only profit was from the put premium. It’s not so offensive compared to the situation when there would be an order to buy futures at the level of 1700. It is also possible for the price to go below the strike and then return above the strike on the option expiration date. In this case, there will be no position in the futures, and only the premium will be earned.

There are statistical characteristics of the underlying asset (futures). Current characteristics differ from average values. The intention is to try to make money on the current market situation.

Solution.Using options on the underlying asset, a strategy for exploiting the statistical characteristics of the market is built.

El rango de precios diario promedio del último mes excede los rangos diarios de los últimos dos días. Se compran opciones a corto plazo, que pueden generar ganancias si aumenta el rango de precios diario.

Existe una amplia gama de estrategias de opciones que deben administrarse de forma dinámica y que pueden adaptarse a las necesidades específicas del operador/inversor.

Necesita suficiente experiencia con carteras de opciones y un conocimiento profundo de las propiedades de las opciones para implementar estrategias de opciones a lo largo del tiempo. Solo especialistas altamente calificados pueden garantizar la ejecución de alta calidad de tales estrategias.

Existe una estrategia de inversión a largo plazo, incluida una implementada a través de futuros. Las ventas dinámicas tácticas de opciones sobre estos futuros son posibles para recibir primas de opciones como posibles ingresos adicionales.

Solución.Se está desarrollando una estrategia individual utilizando opciones

Históricamente, las opciones sobre algunas clases de activos, especialmente los índices bursátiles, han tenido un precio excesivo. Esto implica una posible ventaja para vender volatilidad. Pero hay sutilezas y matices.

Solución.Se está desarrollando una estrategia individual utilizando opciones.

Una vez que se ha iniciado una posición, su visión del mercado puede cambiar.

Solución.Las opciones le permiten cambiar dinámicamente la composición de su cartera para adaptarse a las cambiantes opiniones del mercado. Al mismo tiempo, no hay una necesidad constante de cerrar completamente la cartera inicial. Basta con abrir posiciones adicionales o cambiar las existentes.

Formule sus deseos, incluidas las áreas problemáticas al operar, e intentaremos mejorar la situación.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd está autorizado y regulado por la Comisión de Bolsa y Valores de Chipre de conformidad con la licencia No.281/15 emitida el 25/09/2015. La marca comercial" Just2Trade " es propiedad de Lime Trading (CY) Ltd.

Registration Number: HE 341520

Address: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Información adicional:

Todas las promociones, materiales e información de este sitio web pueden tener condiciones aplicadas. Favor de contactar a la compañía para cualquier detalle

Invertir en mercados financieros contrae riesgos. El valor de la inversión puede tanto incrementar como disminuir y puede causar la perdida del capital del inversionista. En el caso de productos con apalancamiento, la pérdida puede ser mayor al capital invertido. Información detallada sobre los riesgos asociados con invertir en mercados financieros puede ser encontrada en full risk disclosure..

E-mail: 24_support@just2trade.online